Navigating the Future of Sustainable Packaging: A Deep Dive into the Linerless Labels Market

- prajwal79

- May 18

- 6 min read

In today's rapidly evolving commercial landscape, industries worldwide are facing a dual challenge: maximizing operational throughput while drastically reducing environmental footprints. As e-commerce, logistics, and retail sectors scale to meet unprecedented global demand, traditional packaging materials are coming under intense scrutiny. Among these, standard pressure-sensitive labels which rely on a silicone-coated backing liner that is immediately discarded into landfills represent a significant source of industrial waste.

Enter linerless labels. By eliminating the backing liner entirely, this innovative packaging technology offers a streamlined, eco-friendly, and highly efficient alternative. The linerless labels market is experiencing robust acceleration, positioning itself as a cornerstone of modern sustainable supply chains. This comprehensive analysis explores the market's current trajectory, core growth drivers, underlying dynamics, localized regional trends, and future horizons.

Global Market Overview

The global linerless labels market is undergoing a structural transition driven by corporate sustainability mandates and a pressing need for operational optimization. Traditionally, labels require a release liner to prevent the adhesive from sticking to itself when wound on a roll. Linerless labels bypass this requirement by applying a special release coating directly to the face of the label material, allowing the tape-like roll to be wound tightly without adhesion issues.

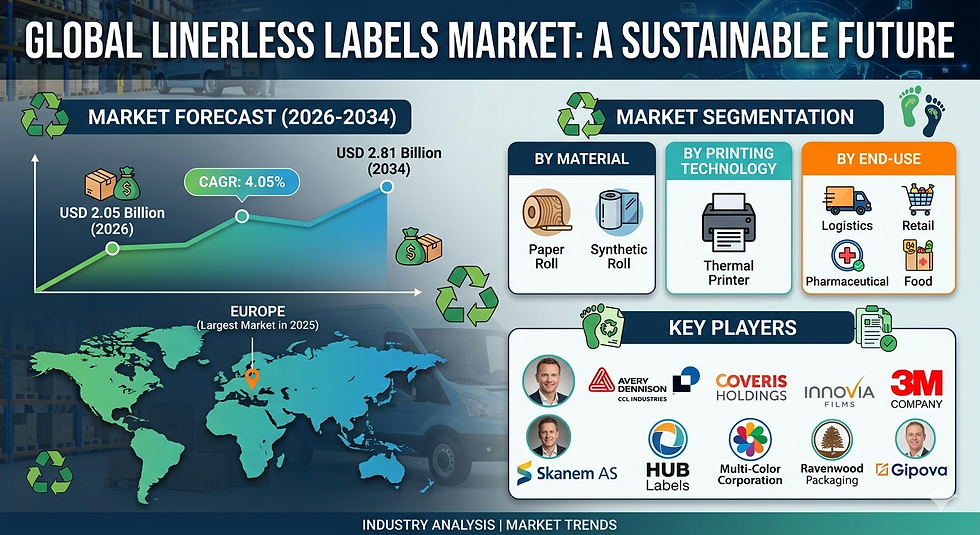

Market valuations indicate a multi-billion-dollar valuation with a highly favorable trajectory. In 2026, the global linerless labels market size is valued at USD 2.05 Billion. Moving forward, the industry is projected to reach a market size of USD 2.81 Billion by 2034, expanding at a Compound Annual Growth Rate (CAGR) of 4.05% during the forecast period from 2026 to 2034.

This steady expansion is heavily underscored by the meteoric rise of the e-commerce sector, strict international environmental regulations, and a widespread shift toward automated logistics. From variable data printing in warehousing to prime labeling in the food and beverage industry, linerless technology is rapidly capturing market share from legacy labeling formats.

Key Market Growth Drivers

The sustained upward trajectory of the linerless labels market is propelled by several macro- and micro-economic factors:

The E-Commerce Explosion: The continuous global surge in online shopping necessitates highly efficient, high-volume shipping and logistics frameworks. Linerless labels enable fulfillment centers to print variable-sized shipping labels seamlessly, speeding up the dispatch process.

Corporate Sustainability and Zero-Waste Targets: Global conglomerates and small-to-medium enterprises alike are committing to net-zero carbon goals. Transitioning to linerless labeling directly eliminates hundreds of tons of solid backing waste, supporting corporate ESG (Environmental, Social, and Governance) compliance.

Enhanced Operational Efficiency: Because a linerless label roll contains up to 40% to 60% more labels per roll compared to standard linered rolls, machinery requires fewer roll changes. This significantly minimizes operational downtime in fast-paced manufacturing and packaging lines.

Reduced Transportation and Storage Costs: Without the bulk of the backing liner, the weight and volume of label rolls are drastically reduced. This allows companies to store more inventory in less space and reduces freight costs, contributing directly to bottom-line savings.

Advancements in Variable-Length Printing: Modern thermal printers can automatically cut a linerless label to the precise size needed for the data printed. This cuts down on material waste, as a single roll can adapt to varying packaging sizes without requiring different pre-cut label stocks.

𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐓𝐡𝐞 𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐞 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐇𝐞𝐫𝐞:

Key Market Dynamics

The mechanics governing the linerless labels market reflect an ecosystem caught between technological innovation, raw material shifts, and evolving consumer demands:

Technological Integration with Thermal Printing: The adoption of linerless labels is inherently tied to hardware compatibility. Market growth is closely mirrored by advancements in direct thermal printing systems configured with specialized cutters and non-stick internal components.

Adhesive and Coating Innovations: The market relies heavily on chemical innovations, particularly UV-curable silicone release coatings and advanced hot-melt or acrylic pressure-sensitive adhesives. Striking the perfect balance between high-tack adhesion and smooth unrolling is a primary focus for manufacturers.

Regulatory Pressures on Single-Use Plastics: Regulatory bodies worldwide are cracking down on packaging waste. Extended Producer Responsibility (EPR) laws are forcing consumer packaged goods (CPG) companies to re-evaluate their entire packaging anatomy, heavily favoring linerless architectures.

Fluctuations in Raw Material Costs: The supply chains for paper, synthetic films (like PP, PE, and PET), and specialized chemicals are subject to macroeconomic volatility, which directly influences the manufacturing margins of label converters.

Market Segmentation

To understand the granular opportunities within this space, the market can be segmented by material type, printing technology, and end-use industry:

By Material Type

Paper: Holds a dominant share of the market due to cost-effectiveness, ease of printability, and widespread application in logistics, logistics tracking, and retail receipts.

Synthetics (Plastics/Films): Gaining rapid traction in environments requiring water resistance, chemical durability, and temperature resilience, such as food processing, pharmaceutical tracking, and outdoor industrial logistics.

By Printing Technology

Direct Thermal: The most prevalent technology used alongside linerless labels. It eliminates the need for ink ribbons, creating an exceptionally clean, low-maintenance, and low-waste printing ecosystem ideal for shipping and retail.

Flexographic and Digital Printing: Primarily utilized for prime or decorative linerless labels where high-vibrancy graphics and corporate branding are paramount.

By End-Use Industry

Logistics and Transportation: The primary engine of volume growth, relying heavily on automated print-and-apply linerless systems for cross-docking and shipping.

Food and Beverage: Heavily utilizes linerless wrap labels for ready-meals, meat trays, and fresh produce due to clean aesthetics, space for regulatory nutritional data, and tamper-evident capabilities.

Retail: Deployed for shelf-edge labeling, weight-scale labeling in delis, and mobile point-of-sale receipting.

Pharmaceuticals and Healthcare: Increasingly adopted for laboratory tracking and prescription labeling where accuracy and sterility are critical.

Country-Wise Analysis and Regional Trends

The adoption rate and market characteristics of linerless labels vary significantly across geographic boundaries:

Europe: Europe held the position of the largest market in 2025. This regional dominance is driven by stringent environmental frameworks, aggressive corporate zero-waste mandates, and pioneering adoption of linerless wrap labels within the UK, German, and French food retail sectors.

United States: The U.S. commands a massive share of the North American market, driven by an unyielding e-commerce infrastructure dominated by logistics giants. High labor costs within the country heavily incentivize automated packaging systems, driving rapid integration of print-and-apply linerless machinery.

United Kingdom: Driven by nationwide plastic pacts, UK retailers have been pioneers in adopting linerless wraps for the food and beverage industry, particularly for ready-to-eat meals.

Germany: As an industrial and manufacturing powerhouse, Germany focuses heavily on precision engineering and logistics automation. German businesses prioritize the operational efficiencies such as reduced downtime and freight optimization offered by linerless technologies.

Japan: Renowned for advanced packaging aesthetics and strict waste management protocols, Japanese markets favor highly advanced, compact linerless systems used across convenience store networks and complex pharmaceutical supply chains.

China: Positioned as a hyper-growth market, China’s massive manufacturing output and exploding domestic e-commerce networks present unparalleled volume opportunities. Government initiatives targeting green logistics are gradually turning the tide toward linerless adoption.

India: While traditionally a price-sensitive market reliant on standard labels, India is witnessing a notable shift. The modernization of organized retail, expansions in cold chain logistics, and intensifying regulatory focus on plastic waste are encouraging top-tier domestic manufacturers to explore linerless alternatives.

Market Challenges and Opportunities

While the market benefits from a strong tailwind, navigating its landscape requires a balanced understanding of its hurdles and prospective breakthroughs:

Challenges

High Initial Capital Expenditure: Upgrading legacy packaging lines to support linerless labeling requires specialized direct thermal printers equipped with non-stick rollers and heavy-duty cutting blades, which can pose a barrier to entry for smaller enterprises.

Adhesive Buildup and Maintenance: Because the adhesive comes into direct contact with the printer's cutting mechanism, accumulation of residue can occur if equipment is not regularly cleaned, potentially leading to mechanical jams.

Limited Custom Shapes: Unlike conventional die-cut labels that can be cut into intricate shapes on a liner, linerless labels are typically restricted to square or rectangular formats due to the inline cutting mechanisms of the printers.

Opportunities

Development of Biodegradable and Compostable Solutions: A massive opportunity lies in synthesizing fully compostable adhesives and face stocks, creating a truly circular packaging product that appeals directly to eco-conscious brands.

Expansion into Emerging Economies: Mid-tier manufacturing hubs across Southeast Asia and Latin America are undergoing rapid supply chain modernization, presenting a blank canvas for linerless label providers.

Smart Label Integration: Merging linerless label manufacturing with RFID or NFC technology opens up high-growth avenues in premium asset tracking, anti-counterfeiting, and intelligent logistics.

Key Market Companies

The competitive matrix of the linerless labels market features a blend of established global packaging conglomerates and highly specialized material science firms. Prominent innovators pushing the boundaries of this technology include:

Avery Dennison Corporation

CCL Industries Inc.

Cenveo Corporation

Constantia Flexibles Group GmbH

Coveris Management GmbH

Fort Dearborn Company

Herma GmbH

Mondi Group

Multi-Color Corporation

SATO Holdings Corporation

UPM Raflatac (UPM)

These industry leaders focus heavily on strategic mergers, geographical expansions, and collaborative R&D ventures alongside printer manufacturers to create harmonized, turnkey labeling systems.

Future Outlook

The trajectory of the linerless labels market points toward a future where sustainable labeling is no longer an optional premium, but an industry standard. As printer modifications become more cost-effective and adhesive chemistries minimize maintenance concerns, the barrier to adoption will continue to fall.

With a projected steady growth reaching USD 2.81 Billion by 2034, the market reflects a permanent shift in packaging design philosophy. Over the next decade, expect a deeper integration of smart technologies into linerless formats alongside a shift toward completely bio-based materials. For brands looking to insulate their operations against tightening environmental regulations while capturing immediate logistics and warehousing efficiencies, investing in linerless labeling systems represents a highly strategic, future-proof imperative.

Comments