Polypropylene Market Projected to Reach USD 246.77 Billion by 2034, Growing at a 6.22% CAGR

- prajwal79

- 2 days ago

- 4 min read

The global material science landscape is witnessing a transformative era, with polypropylene (PP) emerging as a cornerstone of industrial innovation. Known for its versatility, durability, and cost-effectiveness, this thermoplastic polymer is no longer just a "packaging plastic." It has become a critical component in the evolution of lightweight vehicles, sterile medical equipment, and high-performance electronics.

Market Overview

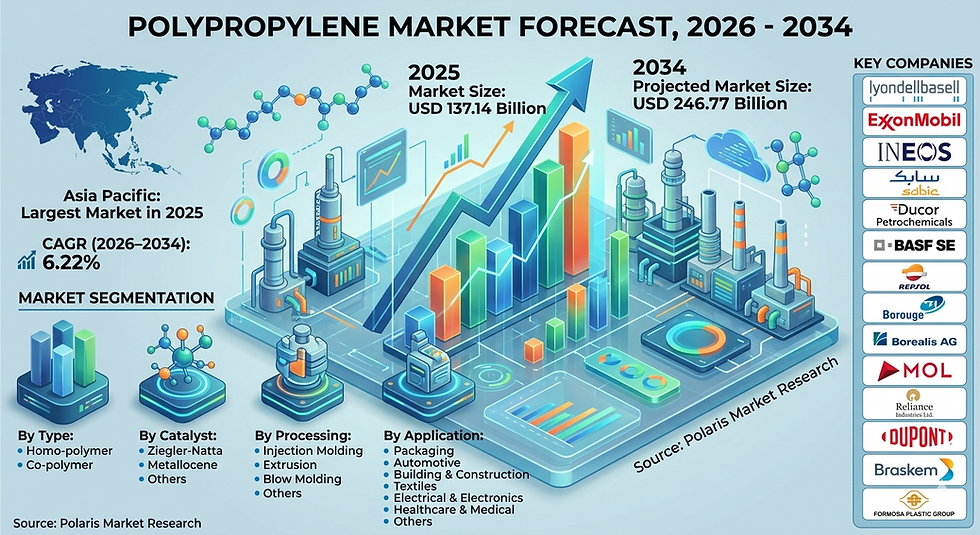

The global polypropylene market is currently on a robust growth path. In 2025, the market was valued at approximately USD 137.14 billion. With a projected Compound Annual Growth Rate (CAGR) of 6.22%, the industry is expected to reach a staggering USD 246.77 billion by 2034.

This growth is largely attributed to the material's unique physical properties low density, high melting point, and excellent chemical resistance making it the material of choice for manufacturers seeking to balance performance with economic efficiency. Currently, the Asia Pacific region dominates the landscape, holding over 36% of the total revenue share, followed by steady expansion in North America and Europe.

Key Market Growth Drivers

Several pivotal factors are accelerating the adoption of polypropylene across diverse sectors:

Lightweighting in the Automotive Industry: As global regulations on carbon emissions tighten, automakers are replacing heavy metal components with high-performance PP to reduce vehicle weight and improve fuel efficiency.

Expansion of the Packaging Sector: The surge in e-commerce and the demand for "on-the-go" food products have heightened the need for rigid and flexible packaging that offers superior moisture barriers and durability.

Healthcare Infrastructure Modernization: Polypropylene’s ability to withstand sterilization processes makes it indispensable for medical devices, syringes, and labware, especially in emerging economies.

Urbanization and Infrastructure: Rising construction activities, particularly in India and China, are driving the demand for PP-based pipes, fittings, and insulation materials.

Key Market Dynamics

The market is characterized by a shift toward sustainability and technological integration:

Sustainability Pivot: There is a growing industry-wide shift toward "Circular Economy" models, focusing on mechanical and chemical recycling of polypropylene to minimize plastic waste.

Technological Advancements: Innovations in catalyst technology (such as Metallocene catalysts) are allowing manufacturers to produce PP with enhanced clarity and impact resistance.

Bio-based Alternatives: Increased R&D investment is flowing into bio-polypropylene derived from renewable feedstocks like vegetable oils, catering to the environmentally conscious consumer base.

𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐓𝐡𝐞 𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐞 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐇𝐞𝐫𝐞:

Market Challenges and Opportunities

While the outlook is positive, the industry must navigate certain hurdles to unlock new potential:

Challenges:

Feedstock Volatility: Since polypropylene is a derivative of crude oil and natural gas (via propylene), fluctuations in global energy prices directly impact manufacturing costs.

Environmental Regulations: Increasingly stringent bans on single-use plastics in various jurisdictions pose a threat to traditional PP packaging segments.

Opportunities:

Electric Vehicle (EV) Boom: The transition to EVs provides a massive opportunity for PP in battery housings and specialized interior components that require high dielectric strength.

Recycling Infrastructure: Companies that invest in advanced recycling technologies can capture a premium market segment dedicated to "green" plastic solutions.

Market Segmentation

The polypropylene market is highly diversified, categorized by polymer type, process, and end-use:

By Polymer Type: Includes Homopolymer (high strength/stiffness) and Copolymer (enhanced flexibility and impact resistance).

By Process: Injection Molding (the largest segment at ~45.8% share), Blow Molding, and Extrusion.

By End-User: Key sectors include Packaging, Automotive, Building & Construction, Electrical & Electronics, and Healthcare.

Country-Wise Analysis and Trends

The geographical distribution of the market reveals distinct regional priorities:

China: As the world’s manufacturing hub, China is the largest consumer of PP. Trends here focus on massive infrastructure projects and a rapidly growing domestic consumer electronics market.

India: Boasting the third-largest automotive market globally, India’s demand is fueled by vehicle production and a government push for improved sanitation and piping infrastructure.

United States: The trend in the U.S. is heavily centered on "Green Chemistry." The Biden-Harris Administration's national strategy to tackle plastic pollution is pushing manufacturers toward advanced recycling and sustainable packaging.

Germany & Turkey: These nations serve as critical hubs for the European automotive and textile sectors, respectively, focusing on high-grade industrial applications of PP.

Saudi Arabia: Remains a dominant exporter, leveraging its vast petrochemical reserves to supply primary forms of polypropylene to global markets.

Key Market Companies

The competitive landscape features a mix of global petrochemical giants and specialized polymer manufacturers:

LyondellBasell Industries N.V.

ExxonMobil Corporation

INEOS

SABIC

Ducor Petrochemicals

BASF SE

Repsol

Borouge

Borealis AG

MOL Group

Reliance Industries Ltd.

Dupont

Braskem

Formosa Plastic Group

These organizations are increasingly focusing on strategic mergers, capacity expansions, and the development of high-performance grades of PP to maintain market leadership.

Future Outlook

The future of the polypropylene market is undeniably tied to the "Green Transition." Over the next decade, we expect to see a decoupling of market growth from virgin fossil fuel consumption. The rise of chemically recycled PP will likely bridge the gap between performance requirements and environmental mandates.

Furthermore, the "Smart Packaging" trend where PP is integrated with sensors for food freshness or pharmaceutical tracking will open new high-value frontiers. For stakeholders, the message is clear: adaptability in the face of sustainability regulations and a focus on high-growth regions like Asia Pacific will be the primary determinants of success in the 2030s.

𝐑𝐞𝐥𝐚𝐭𝐞𝐝 𝐁𝐥𝐨𝐠

Comments