Global Copper Scrap Market Projected to Reach USD 148.44 Billion by 2034, Registering a Robust 8.9% CAGR

- prajwal79

- 2 hours ago

- 7 min read

The transition toward a low-carbon economy relies heavily on securing reliable, sustainable streams of critical industrial base metals. Among these, copper occupies a central role due to its unparalleled electrical and thermal conductivity. As the global community prioritizes sustainability and structural shifts across heavy industries, the secondary metal sourcing sector has emerged as an indispensable cornerstone of manufacturing supply chains.

A definitive study from Polaris Market Research highlights this structural shift, mapping out the trajectories, variables, and structural segmentations defining the global landscape of recycled copper. This comprehensive executive overview evaluates the current performance and long-term future outlook of this vital commodity sector.

Market Overview

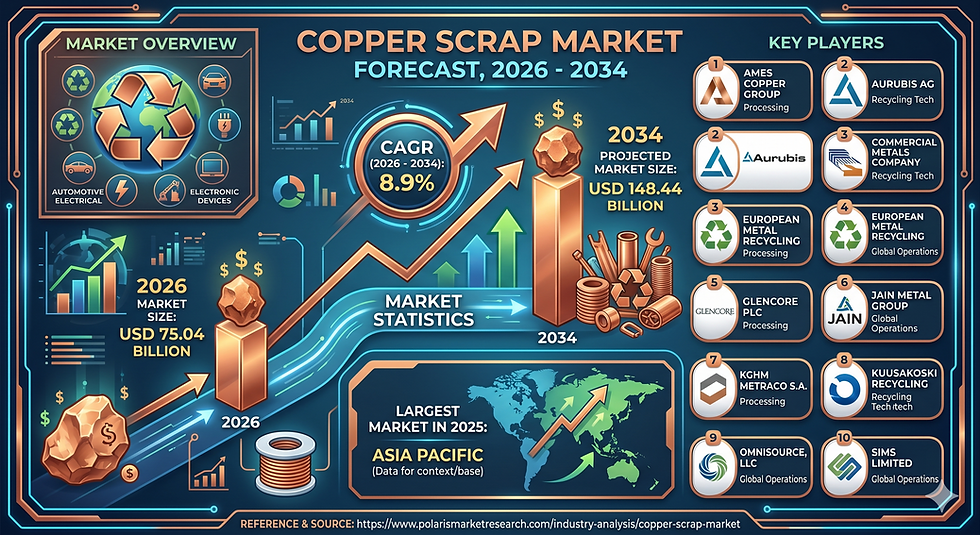

The global copper scrap market is experiencing a prolonged period of expansion, acting as a crucial indicator for both macroeconomic industrial health and the broader adoption of sustainable resource circularity. According to the strategic datasets compiled by Polaris Market Research, the global copper scrap market size was valued at USD 69.17 billion in 2025. Demonstrating robust structural momentum, the industry is projected to reach USD 75.04 billion in 2026.

Fueled by systemic shifts across infrastructure networks, consumer electronics, and green transport, the market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 8.9% over the forecast period spanning 2026 to 2034. By the conclusion of this horizon in 2034, the global market valuation is projected to reach USD 148.44 billion.

This growth curve underscores a foundational transition within manufacturing: secondary copper is no longer viewed merely as a secondary cost-saving fallback, but rather as a primary strategic resource for global industries seeking to optimize supply security, manage input cost volatility, and drastically reduce scope-three upstream emissions.

Key Market Growth Drivers

The significant expansion of the market is underpinned by a series of interconnected structural drivers that span regulatory, economic, and technological landscapes:

Sustainable Circular Economy Mandates: The accelerating global push toward circular economy models and structured corporate sustainability targets serves as a primary catalyst. Regulators and enterprise consumers are moving away from traditional linear consumption frameworks to mitigate ecological depletion.

Reduced Carbon and Energy Footprints: Processing secondary copper scrap requires significantly less energy compared to extracting, milling, and refining primary copper from newly mined ore. This energy efficiency helps industrial operators lower their carbon emissions and meet strict environmental compliance standards.

Surging Downstream Industrial Demand: The ongoing expansion of core industrial sectors, most notably heavy electrical engineering, electronic device fabrication, and modern building construction, maintains a high demand for available copper scrap.

Financial Viability Against Primary Ore Volatility: Rising exploration costs, declining copper ore grades globally, and the capital-intensive nature of primary mining make secondary scrap a highly competitive, affordable, and economically stable raw material choice.

Rapid Infrastructure and Urban Transitions: Global urbanization necessitates extensive upgrades to metropolitan power grids, localized telecommunication networks, and structural real estate, ensuring a continuous demand for conductive components.

Key Dynamics

The operational framework of the global secondary copper landscape is shaped by dynamic interactions between supply chain logistics, technological advancements, and economic realities:

Strategic Integration of Green Technologies: The widespread deployment of green technologies, such as electric vehicle (EV) architectures, localized battery storage systems, and renewable utility grids, relies heavily on high-purity copper. Utilizing recycled scrap provides a sustainable pathway to fulfill these resource-heavy initiatives.

Supply Loop Infrastructure Maturity: The market benefits from well-developed, institutionalized scrap collection networks. This mature infrastructure ensures a steady return of post-consumer and pre-consumer scrap back into industrial production loops.

Urban Mining Efficiency: The continuous decommissioning of obsolete urban infrastructure, old plumbing systems, and end-of-life industrial machinery acts as an ongoing supply source, minimizing reliance on overseas raw material imports.

Quality Retention Profiles: Copper possesses the unique metallurgical property of being endlessly recyclable without experiencing any degradation in physical strength, performance, or electrical conductivity, making it an ideal candidate for closed-loop recycling.

Secondary Refining Capacity Adjustments: Smelters and secondary refiners worldwide are actively upgrading their production configurations to process broader variations of contaminated secondary feeds, shifting balance away from primary concentrates.

𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐓𝐡𝐞 𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐞 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐇𝐞𝐫𝐞:

Market Challenges and Opportunities

Operating within a complex global trading framework, the secondary copper sector faces a distinct set of operational challenges alongside emerging market opportunities:

Challenges:

Varied Scrap Composition and Scrap Impurities: While certain premium grades offer straightforward processing, significant portions of available scrap consist of complex alloys or materials mixed with coatings, solder, and plastics. This requires extensive, multi-staged processing and sorting to achieve required purity levels.

Technical Processing Complexities: Removing deeply embedded contaminants from low-grade scrap requires advanced sorting technologies and multi-staged secondary smelting configurations, which can elevate processing costs for regional operators.

Regulatory Restrictions on Global Waste Trade: Stringent cross-border regulations, strict compliance standards for transboundary waste movements, and shifting scrap import/export quotas present ongoing challenges for international supply chains.

Opportunities:

Advanced Sorting Technology Deployment: Deploying automated sorting technologies, such as sensor-based sorting, advanced X-ray transmission, and AI-driven optical systems, offers significant potential to optimize recovery yields from highly complex mixed scrap streams.

Domestic Secondary Refining Infrastructure Upgrades: Developing advanced regional smelting plants capable of directly converting low-grade scrap into high-purity secondary refined copper presents a major growth opportunity, particularly in regions aiming to reduce dependence on external refining.

Structural Upstream Industry Collaborations: Establishing formal, direct buy-back agreements and closed-loop recycling partnerships between scrap processors and major industrial end-users (such as automotive OEMs and electronics manufacturers) creates highly secure, predictable supply channels.

Market Segmentation Insights

The structural organization of this industry is best understood through its key segments, which define how material flows from origin to end-use:

Feed Material:

The market is divided primarily into New Scrap, Old Scrap, and Secondary Refined Copper. Old scrap, derived from end-of-life products like obsolete electronics, buildings, and retired vehicles, held a substantial market share of 45.3% in 2025. This leading position is driven by the vast, continuous supply generated by ongoing product obsolescence and demolition activities.

Scrap Grade:

Classifications include Bare Bright Copper, #1 Copper Scrap, #2 Copper Scrap, and other alloyed variants. The #2 copper scrap segment accounted for 19.7% of the global revenue share in 2025. Despite requiring more intensive processing to eliminate coatings and impurities, its widespread availability in common plumbing and electrical systems makes it a highly reliable resource for the recycling sector.

Application:

Key industrial processing routes include Wire Rod Mills, Brass Mills, Ingot Makers, and Foundries. Wire rod mills represent the largest application segment, holding a 34.79% market share in 2025. This dominance is directly tied to the global demand for newly extruded electrical wiring, rods, and cabling across infrastructure projects.

End Use:

Downstream consumption is distributed across Building & Construction, Electrical & Electronics, Industrial Machinery, Transportation Equipment, and Consumer Products. The electrical & electronics segment leads this category, capturing approximately 28% of total market revenue. This position is sustained by the continuous production of transformers, power transmission lines, complex circuit boards, and consumer devices.

Country-Wise Market Trends and Regional Analysis

An assessment of global geographic dynamics reveals distinct trends and varying levels of infrastructure maturity across key regions:

Asia Pacific:

Asia Pacific stands as the dominant force in the global landscape, holding an impressive 61.43% of total market revenue share in 2025. The region's leading position is sustained by massive rates of urbanization and rapid industrialization across major manufacturing hubs. Boasting extensive processing networks and substantial consumption capacity, the regional market continues to drive global scrap flows to feed its expansive electronics and building construction sectors.

North America:

The North American market remains a major, highly institutionalized player within the global secondary metal trade. Industry dynamics here are characterized by a steady supply of old scrap from large-scale commercial demolition alongside a continuous stream of new scrap from domestic manufacturing plants. Supported by advanced collection logistics and well-developed regulatory frameworks, the region excels in collecting high-purity scrap grades like bare bright and #1 copper.

Europe:

Europe continues to be a highly progressive region for secondary copper utilization, heavily supported by strict circular economy policies, carbon neutrality mandates, and institutionalized recycling frameworks. European industrial consumers prioritize high-grade secondary refined copper to meet ambitious corporate sustainability targets and minimize carbon import taxes. The regional ecosystem focuses on upgrading secondary smelting technologies to manage complex post-consumer scrap arrays locally.

Middle East & Africa:

The Middle East market demonstrates notable growth, valued at USD 304.71 million in 2024 and projected to reach USD 575.75 million by 2034, expanding at a CAGR of 6.6% from 2025 to 2034. Growth in this region is primarily driven by large-scale infrastructure projects and major real estate developments, particularly within Saudi Arabia, which holds the dominant position in the Middle East market due to its rapid infrastructure expansion.

Latin America:

Latin America represents an emerging segment focused primarily on enhancing its export potential and improving basic collection networks. As local manufacturing capacities expand and mining states look to diversify metal production pathways, the development of localized scrap collection centers is gaining traction, providing secondary feed materials to both regional and international markets.

Market Key Companies

The competitive landscape of the global copper scrap industry features a mix of multinational mining enterprises, dedicated recycling conglomerates, and specialized secondary refiners. Prominent organizations shaping market dynamics and driving infrastructure investments include:

Aurubis AG

Sims Limited

Glencore PLC

Commercial Metals Company

OmniSource, LLC

Ames Copper Group

Jain Metal Group

European Metal Recycling

Kuusakoski Recycling

KGHM METRACO S.A.

These industry leaders focus heavily on expanding processing capacities, integrating advanced automated sorting technologies, and securing strategic supply loops with upstream industrial manufacturing partners to ensure consistent feed volumes.

Future Outlook

The long-term outlook for the global copper scrap market points toward sustained, structural integration within the wider industrial base metal supply chain. Moving toward 2034, the reliance on secondary sourcing is expected to intensify as primary extraction faces increasing headwinds from declining ore purity, strict environmental regulations, and high capital costs.

Technological innovation will play a critical role in this evolution. The broader adoption of artificial intelligence, advanced optical sorting systems, and specialized secondary smelting processes will allow recycling networks to process lower-grade, highly complex scrap materials efficiently. This will help close the supply-demand gap for premium conductive metals.

As regional economies look to secure their raw material supply chains and minimize external dependencies, localized scrap collection and processing will become increasingly vital to national economic strategies. Backed by solid market fundamentals, an anticipated CAGR of 8.9%, and an expanding range of applications in green technologies, the copper scrap industry is well-positioned to remain an essential component of the global manufacturing economy.

Comments